Are you ready to take the leap into homeownership? Before you start house hunting, it's crucial to understand the importance of a home loan pre-approval checklist. This essential tool can streamline the home-buying process, giving you a clear idea of your budget and enhancing your bargaining power with sellers. By following a comprehensive checklist, you can avoid potential pitfalls and ensure a smooth transition from prospective buyer to proud homeowner.

Home loan pre-approval is a proactive step that puts you in the driver's seat of your home-buying journey. It involves a thorough evaluation of your financial standing, creditworthiness, and borrowing capacity by a lender. This process not only helps you understand how much you can afford but also demonstrates your seriousness to sellers and real estate agents. With a pre-approval in hand, you can confidently make offers, negotiate better terms, and secure your dream home.

In this article, we'll delve into the intricacies of the home loan pre-approval checklist, providing a step-by-step guide to help you navigate this critical stage. From gathering necessary documents to understanding credit scores, we'll cover everything you need to know. Whether you're a first-time buyer or a seasoned investor, our detailed checklist will equip you with the knowledge and confidence to make informed decisions and achieve your homeownership goals.

Read also:Byddy Vs Byddf A Comprehensive Analysis

Table of Contents

- What is Home Loan Pre-Approval?

- Why is Home Loan Pre-Approval Important?

- What Documents Are Needed for Pre-Approval?

- Understanding Credit Score Requirements

- How Does the Income Verification Process Work?

- Employment History and Stability

- Assessing Your Debt-to-Income Ratio

- How to Choose the Right Lender?

- Key Questions to Ask Your Lender

- Common Mistakes to Avoid in Pre-Approval

- Checking Your Credit Report for Errors

- Impact of Pre-Approval on Your Home Search

- The Ultimate Home Loan Pre-Approval Checklist

- Frequently Asked Questions

- Conclusion

What is Home Loan Pre-Approval?

Home loan pre-approval is a preliminary assessment conducted by a lender to determine a borrower's eligibility for a mortgage. This process involves evaluating the borrower's financial situation, including income, credit score, employment history, and other relevant factors. It's not a guarantee of a loan but an indication of the amount a lender is willing to offer based on the information provided.

When you apply for pre-approval, the lender will review your financial documents, run a credit check, and assess your borrowing capacity. This pre-approval serves as a conditional commitment, outlining the terms and conditions under which the lender is willing to extend a home loan. It's important to note that pre-approval usually has an expiration date, typically lasting between 60 to 90 days.

Having a pre-approval letter in hand provides several advantages. It shows sellers and real estate agents that you're a serious buyer, ready to make a competitive offer. It also helps you establish a clear budget, preventing you from overextending financially. Additionally, it can expedite the final loan approval process once you've found your desired property.

Why is Home Loan Pre-Approval Important?

Understanding the importance of home loan pre-approval is crucial for any prospective homebuyer. Firstly, it provides clarity and confidence, allowing you to focus your search on properties within your financial reach. By knowing your borrowing capacity, you can avoid the disappointment of falling in love with a home that is out of your budget.

Moreover, pre-approval can significantly enhance your negotiating power. Sellers are more likely to take your offer seriously when they see that you're pre-approved for a mortgage. This can give you an edge in competitive markets, where multiple buyers are vying for the same property.

Another key benefit is the ability to identify and address potential issues early. During the pre-approval process, the lender might uncover discrepancies or issues in your financial profile that could hinder your loan approval. By resolving these matters upfront, you can improve your chances of securing a mortgage when it matters most.

Read also:Shameless 1st Season Cast The Dynamic Faces Driving The Iconic Showtime Series

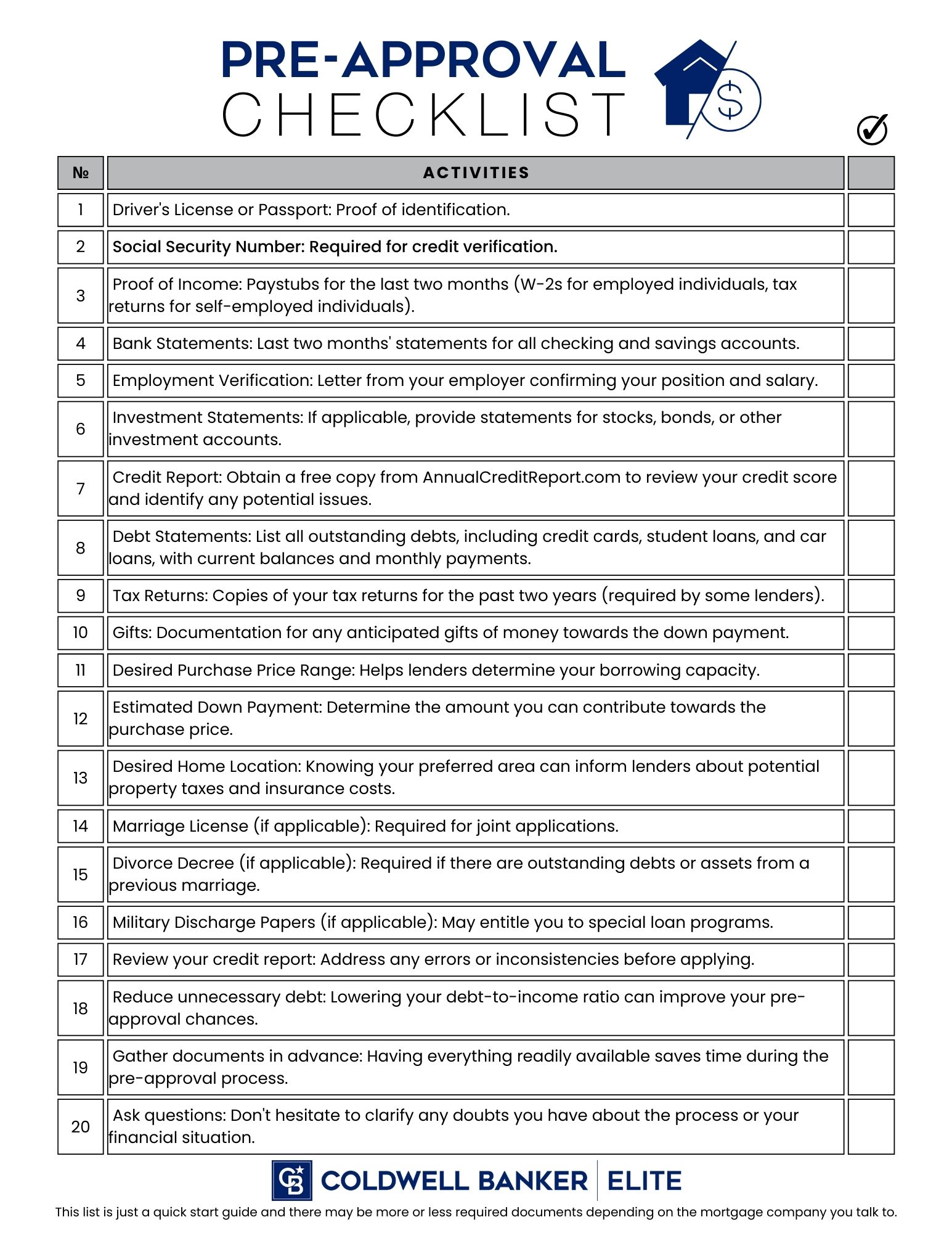

What Documents Are Needed for Pre-Approval?

Preparing the necessary documents for home loan pre-approval is a critical step in the process. Gather the following items to ensure a smooth and efficient evaluation:

- Identification: Valid government-issued ID (e.g., driver's license, passport)

- Income Proof: Recent pay stubs, W-2 forms, or tax returns

- Employment Verification: Letters from employers or contact information for verification

- Bank Statements: Recent statements from all accounts to verify savings and assets

- Credit Report: A current copy of your credit report to evaluate your creditworthiness

- Debt Information: Documentation of existing debts (e.g., credit card statements, loan agreements)

- Rental History: If applicable, records of rental payments or a letter from your landlord

Having these documents ready will expedite the pre-approval process and demonstrate your preparedness to lenders. It's essential to ensure all information is accurate and up-to-date to avoid delays or complications.

Understanding Credit Score Requirements

Your credit score plays a pivotal role in the home loan pre-approval process. Lenders use this score to gauge your creditworthiness and assess the risk of lending to you. Generally, a higher credit score translates to better loan terms, lower interest rates, and a higher likelihood of approval.

Most lenders require a minimum credit score of around 620 for conventional loans, while government-backed loans, such as FHA loans, may have lower requirements. However, it's important to note that individual lenders might set their own criteria, so it's advisable to check with multiple lenders to understand their specific requirements.

If your credit score falls below the desired threshold, consider taking steps to improve it before applying for pre-approval. This could involve paying down existing debts, correcting errors on your credit report, or establishing a consistent history of on-time payments.

How Does the Income Verification Process Work?

Income verification is a fundamental aspect of home loan pre-approval. Lenders need to ensure that you have a stable and sufficient income to meet your mortgage obligations. The process typically involves the following steps:

- Submission of Income Documents: Provide recent pay stubs, tax returns, and W-2 forms to verify your income sources.

- Employment Verification: Lenders may contact your employer to confirm your employment status, position, and salary.

- Assessment of Additional Income: If you have other income streams (e.g., rental income, investments), provide documentation to support these claims.

Accurate and thorough income verification is critical to demonstrating your ability to repay the loan. Be prepared to explain any fluctuations in income or gaps in employment history, as this could impact the lender's decision.

Employment History and Stability

Lenders place a strong emphasis on employment history and stability when evaluating loan pre-approval applications. A consistent work history with a stable employer indicates reliability and reduces the perceived risk for lenders.

Typically, lenders prefer applicants who have been in their current job for at least two years. However, if you've recently changed jobs, it's not necessarily a deal-breaker. Providing evidence of continuous employment in the same industry or a higher-paying role can mitigate concerns.

If you have gaps in your employment history, be prepared to explain the reasons and provide documentation where applicable. This could include letters from previous employers, documentation of freelance work, or records of any professional development undertaken during these periods.

Assessing Your Debt-to-Income Ratio

The debt-to-income (DTI) ratio is a critical measure that lenders use to evaluate your financial health and ability to manage additional debt. It compares your monthly debt obligations to your gross monthly income, providing a snapshot of your financial commitments.

To calculate your DTI ratio, add up your monthly debt payments (e.g., credit cards, car loans, student loans) and divide the total by your gross monthly income. Multiply the result by 100 to express it as a percentage.

Most lenders prefer a DTI ratio of 43% or lower, although some may accept higher ratios under certain circumstances. A lower DTI ratio indicates a stronger financial position, making you a more attractive candidate for pre-approval.

How to Choose the Right Lender?

Selecting the right lender for your home loan pre-approval is a crucial decision that can impact your entire home-buying experience. Consider the following factors when evaluating potential lenders:

- Interest Rates: Compare rates from multiple lenders to ensure you're getting the best deal.

- Fees and Charges: Review any additional fees, such as origination fees, application fees, or early repayment penalties.

- Customer Service: Assess the lender's reputation for customer service and responsiveness.

- Loan Options: Consider the variety of loan products offered and whether they align with your needs and preferences.

It's advisable to consult with multiple lenders to understand their offerings and receive personalized quotes. This not only helps you make an informed decision but also strengthens your negotiating position by demonstrating that you're an informed and proactive borrower.

Key Questions to Ask Your Lender

Engaging in open and transparent communication with your lender is essential to ensure a smooth pre-approval process. Here are some key questions to ask:

- What are the current interest rates and how can I secure the best rate?

- Are there any fees associated with the pre-approval process?

- What loan products do you offer and which one is best suited to my needs?

- How long does the pre-approval process take and when will I receive a decision?

- Can you explain the impact of my credit score on my loan terms?

- What documentation do you require and how should I submit it?

By asking these questions, you can gain a deeper understanding of the pre-approval process and make informed decisions. This proactive approach also helps build a stronger relationship with your lender, ensuring a smoother home-buying journey.

Common Mistakes to Avoid in Pre-Approval

While home loan pre-approval is an essential step in the home-buying process, several common mistakes can hinder your progress. Avoid the following pitfalls:

- Providing Inaccurate Information: Ensure all documents and information submitted are accurate and up-to-date to prevent delays or denials.

- Overlooking Credit Report Errors: Regularly review your credit report for errors and address any discrepancies promptly.

- Ignoring the Debt-to-Income Ratio: Be mindful of your DTI ratio and work on reducing debt if necessary before applying for pre-approval.

- Neglecting to Compare Lenders: Research multiple lenders and compare their offerings to find the best fit for your needs.

- Making Large Financial Changes: Avoid major financial changes, such as switching jobs or taking on new debt, during the pre-approval process.

By steering clear of these mistakes, you can increase your chances of a successful pre-approval and a smooth transition to homeownership.

Checking Your Credit Report for Errors

Checking your credit report for errors is an essential step before applying for home loan pre-approval. Even small inaccuracies can impact your credit score and affect your borrowing capacity.

Start by obtaining free copies of your credit report from the major credit bureaus: Equifax, Experian, and TransUnion. Review the reports for any inaccuracies, such as incorrect account balances, outdated information, or unfamiliar accounts.

If you identify any errors, contact the credit bureau to dispute the information and request a correction. Be prepared to provide supporting documentation to validate your claim. This proactive approach can help improve your credit score and enhance your pre-approval prospects.

Impact of Pre-Approval on Your Home Search

Securing home loan pre-approval has a significant impact on your home search, providing clarity and confidence as you navigate the market. With a pre-approval letter in hand, you can:

- Focus on Homes Within Your Budget: Avoid wasting time on properties outside your financial reach and concentrate on realistic options.

- Negotiate with Confidence: Present your pre-approval to sellers and real estate agents to demonstrate your seriousness and strengthen your negotiating position.

- Accelerate the Closing Process: Expedite the final loan approval and closing process once you've found the right home, reducing potential delays.

Pre-approval not only streamlines your home search but also reduces stress and uncertainty, allowing you to make informed decisions with peace of mind.

The Ultimate Home Loan Pre-Approval Checklist

To ensure a seamless pre-approval process, follow this comprehensive checklist:

- Gather Necessary Documents: Collect identification, income proof, bank statements, and credit report.

- Review Your Credit Score: Check your credit score and address any issues or discrepancies.

- Calculate Debt-to-Income Ratio: Assess your DTI ratio and take steps to improve it if necessary.

- Research Lenders: Compare interest rates, fees, and loan options from multiple lenders.

- Submit Pre-Approval Application: Complete the application accurately and provide all required documentation.

- Engage with Lenders: Communicate openly with lenders and ask relevant questions to gain clarity.

- Avoid Major Financial Changes: Maintain financial stability and avoid significant changes during the pre-approval process.

By diligently following this checklist, you can enhance your chances of obtaining home loan pre-approval and embark on your homeownership journey with confidence.

Frequently Asked Questions

1. How long is a home loan pre-approval valid?

Pre-approval typically lasts between 60 to 90 days, depending on the lender's policies. It's important to verify the specific timeframe with your lender and renew the pre-approval if needed.

2. Can I apply for pre-approval with multiple lenders?

Yes, you can apply for pre-approval with multiple lenders to compare offers and find the best terms. However, submitting multiple applications within a short period may temporarily impact your credit score.

3. Does pre-approval guarantee a home loan?

No, pre-approval is not a guarantee of a home loan. It indicates a lender's willingness to offer a loan based on the information provided, but final approval depends on property appraisal, underwriting, and other factors.

4. How can I improve my chances of pre-approval?

To improve your chances, maintain a strong credit score, reduce debt, gather accurate documentation, and avoid major financial changes during the pre-approval process.

5. What happens if my financial situation changes after pre-approval?

If your financial situation changes (e.g., job loss, new debt), inform your lender immediately. They may need to reassess your pre-approval based on the updated information.

6. Can pre-approval affect my home search timeline?

Yes, having pre-approval can expedite your home search by allowing you to make competitive offers and speed up the closing process once you find the right property.

Conclusion

In conclusion, a home loan pre-approval checklist is an invaluable tool for aspiring homeowners. By understanding the steps involved, gathering the necessary documents, and engaging with lenders, you can navigate the pre-approval process with confidence. This proactive approach not only enhances your bargaining power but also streamlines your home search, allowing you to focus on finding the perfect home within your budget.

Remember, home loan pre-approval is not just about securing a mortgage; it's about empowering yourself with knowledge and clarity. By following our comprehensive checklist and avoiding common pitfalls, you can increase your chances of success and embark on your homeownership journey with optimism and assurance.

For further guidance and resources on home loan pre-approval, consider consulting with financial advisors or visiting reputable websites such as the Consumer Financial Protection Bureau.